Medical

comprehensive coverage for certain services—including in-network preventive care covered at 100%

The Mondelēz Global Medical Plan (Medical Plan) offers two coverage options, both through the same carrier:

- Two coverage options (see side-by-side comparison below), one of which is paired with a Health Savings Account (HSA). You can use an HSA to help pay for eligible expenses on a tax-free basis (see the HSA page for details).

- One carrier, both coverage options are available through Blue Cross and Blue Shield of Illinois (BCBS).

Log in to your MyBenefits Online account to see your current coverage elections, and for additional coverage and carrier-related details.

Note that both medical coverage options include prescription drug coverage through retail and mail order programs. Prescription drug coverage is through CVS Caremark.

Key Features

The Classic PPO and HSA-Compatible PPO options have key features.

How the coverage options are the same

- Covered services: Both coverage options provide comprehensive coverage for the same medical services, such as doctor office visits and hospital stays.

- Carrier: Both options are available through BCBS, which offers both in-network and out-of-network coverage.

- Preventive care coverage: In-network preventive care is covered at 100% (e.g., annual physical, mammogram, well-child care).

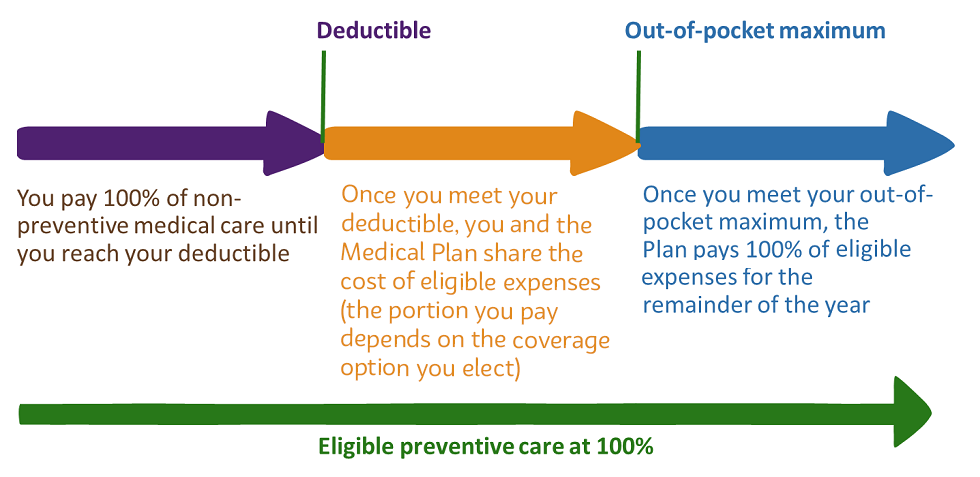

- Medical copay and coinsurance amounts: After reaching the deductible, you pay a portion of the cost for most covered services. That portion is either a flat-dollar amount per service (copay) or a percentage of the cost (coinsurance). Once you reach the out-of-pocket maximum, you pay nothing.

- Prescription drug copay/coinsurance amounts (retail pharmacy): For a 30-day supply, pay a copay for Generic and Preferred Brand prescriptions. For Non-Preferred Brand prescriptions, you pay a copay under the HSA-Compatible PPO option and coinsurance under the Classic PPO option. With the HSA-Compatible PPO, you must satisfy the deductible first before the copay applies. With the Classic PPO option, there’s no deductible for prescription drug coverage so cost sharing applies immediately.

How they are different

Here’s a quick comparison.

| Features | Classic PPO | HSA-Compatible PPO |

| Deductible. You have a lower deductible to meet, so the Medical Plan begins to pay benefits sooner. | ✓ | |

| Copay. After you meet the deductible, you pay a flat-dollar amount toward the cost of each covered service. | ✓ | |

| Coinsurance. After you meet the deductible, you pay a percentage of the cost for each covered service. | ✓ | |

| Save with an HSA. Coverage is paired with an HSA to help pay for out-of-pocket costs and/or save for the future—all tax free. | ✓ | |

| Use the Health Care FSA to save on taxes. Money you don’t use for eligible expenses during the year will be forfeited. | ✓ | |

| Pay the deductible first for prescriptions. You must meet the deductible first before the Medical Plan begins to pay benefits for covered prescription drugs. | ✓ |

About the carrier networks

The carrier has a large selection of network providers, for example doctors and hospitals, across the country. And, when you stay in-network, covered services are provided at a discount.

Here’s a snapshot of the carrier, type of network offered, and the name of the carrier’s network.

| Carrier | Type of Network | Network Name |

|---|---|---|

| Blue Cross and Blue Shield of Illinois (BCBS) | Broad | Blue Card PPO or Blues Alternate Networks |

To confirm whether your doctor, hospital, or other care provider participates in the carrier’s network, be sure to use the provider look-up tool on MyBenefits Online. However, it’s also a good idea to double-check directly with your provider to make sure they participate in the network before you receive care. Your provider will have the most up-to-date information about their network participation.

How you pay for care

To decide what’s right for you, take a close look at your costs and consider how you prefer to pay for coverage.

- Classic PPO means you’ll have higher contributions, but coverage will begin sooner (lower in-network deductible and out-of-pocket maximum).

- HSA-Compatible PPO means your contributions will be lower, but it will take longer for coverage to begin (higher deductible and out-of-pocket maximum).

Here’s how the options compare against some of the key features that affect how and when you pay for care:

| Classic PPO | HSA-Compatible PPO | |

|---|---|---|

| Contributions | Higher | Lower |

| Deductible that must be met up-front | Lower | Higher |

| What the Medical Plan pays after the deductible is met (for most covered services) | Full cost, less you copay | 90% |

| Out-of-pocket maximum amount | Lower | Higher |

Need a quick refresher on how you and the Medical Plan—regardless of whether you select the Classic PPO or HSA-Compatible PPO option—share in the cost of coverage? Check out the graphic below.

Family Coverage

If you cover family members, it’s important to understand how the deductibles and out-of-pocket maximums work—it affects when the Medical Plan’s benefits kick in.

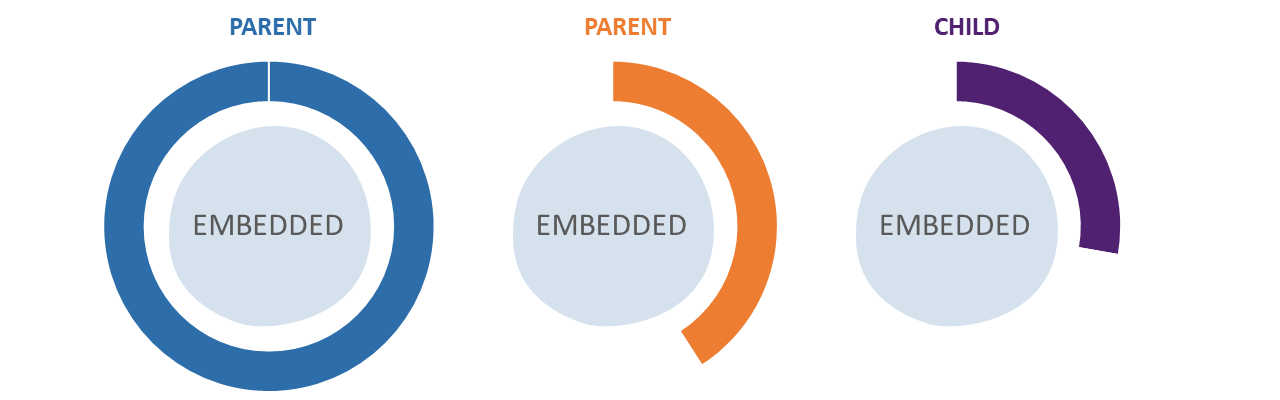

Embedded

The Classic PPO option has an embedded approach to the deductible, which is the more traditional way of thinking about deductibles. With this approach, once one family member meets their individual deductible, it’s considered met for that person. Benefits begin for them, but not yet for the other family members. This means:

- Each person only needs to meet the individual deductible before the Medical Plan begins paying benefits for that individual.

- Other covered family members will continue to pay all of their health care expenses until two or more combined meet the family deductible. When that happens, the Medical Plan then begins paying benefits for all covered family members.

- If you have a family member who tends to have more health care costs than the others, you might want to consider choosing an option with this approach, as it could save you money.

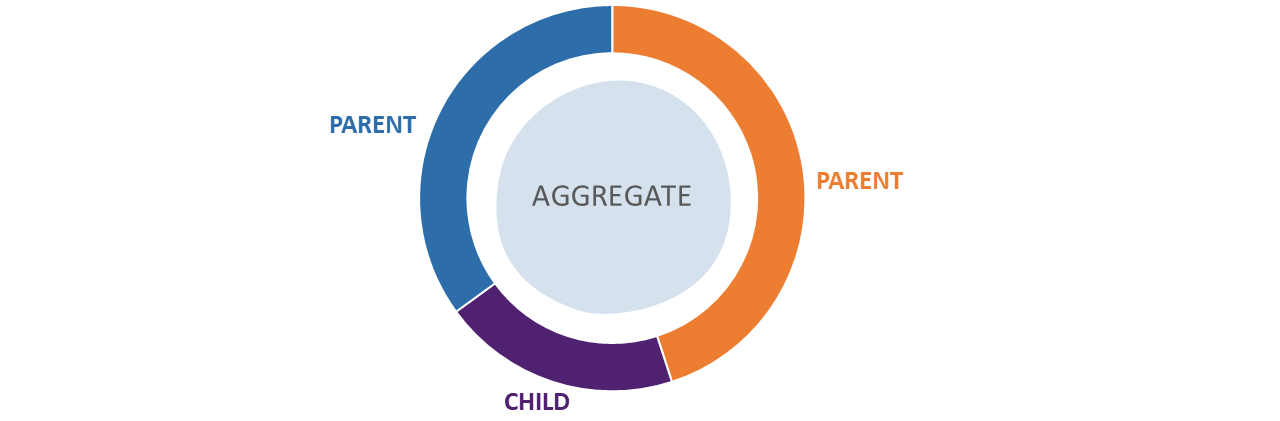

Aggregate

In order to meet IRS rules to be paired with an HSA, the HSA-Compatible PPO option has an aggregate approach to the deductible. With this approach, there’s one deductible for the whole family. This means:

- You ignore the individual deductible amount completely.

- Only the family deductible applies to each covered family member.

- Once one person or a combination of covered family members meet the deductible, it’s considered met for all covered family members and benefits begin for everyone.

The embedded and aggregate methodologies work the same for out-of-pocket maximums as they do for deductibles. Note, however, that even though the HSA-Compatible option’s deductible is aggregate; its out-of-pocket maximum approach is embedded. As a result, both the Classic PPO and HSA-Compatible options have embedded out-of-pocket maximums.

Telemedicine

Both coverage options offer telemedicine. With telemedicine, you can talk to a doctor 24/7 for a variety of services (e.g., general medical, behavioral/mental health). Per-visit costs vary by the type of service received; but are often less than what you would pay for in-office care.

For specifics on telemedicine options and costs, contact the carrier directly at 1-800-770-4622 or access the MD Live Website.

Learn more about telemedicine in this video.

Contact info & apps

Blue Cross and Blue Shield of Illinois (BCBS)

- BCBS of Illinois Website

- MD Live Website

- Main Phone: 1-877-238-5948

- Telemedicine: 1-800-770-4622

- Nurseline: 1-800-299-0274

- Mobile App: APPLE APP STORE | GOOGLE PLAY STORE

- Group Number: See your member ID card

- Network: Broad—Blue Card PPO or Blues Alternate Networks (depending on location)

Medical coverage options: In-Network Benefits*

Both options through BCBS cover certain medical services and prescription drugs. Note that the options differ by price. Before you enroll, use the online tools to help you decide which coverage option works best for you and your family. And, if you have ongoing treatment and your enrollment will result in a carrier change, ask the new carrier about their transition-of-care policy.

| Coverage Option | Classic PPO | HSA-Compatible PPO |

| Available Account | Health Care FSA | Health Savings Account (HSA) |

| Contribution Amount | $$ | $ |

| Note: If applicable, the current contribution amount you pay is on MyBenefits Online | ||

| Preventive Care | Covered at 100% when you use in-network provides (no deductible) | |

| You Pay | ||

| Deductible (Individual/Family) | $500/$1,000 |

$1,650/$3,300

|

| Copay/Coinsurance (After Deductible) | $25 for most covered services | 10% for most covered services |

| Out-of-Pocket Maximum (Individual/Family; Includes Deductible) | $2,750/$5,500 | $4,500/$9,000 |

| Deductible and Out-of-Pocket Maximum Type |

Embedded

|

Aggregate (deductible) and Embedded (out-of-pocket maximum)

|

*Out-of-network benefits are also available, but benefits are lower and your costs are higher. So, it’s worth it to stay in-network. For details, access MyBenefits Online.

More information

You can access more detailed information, including comparisons of the coverage options, on MyBenefits Online.

Short videos you may find helpful

Check out these videos to learn more about how to:

Key Considerations when choosing medical coverage

How and when do you prefer to pay for medical coverage?

- If you prefer to pay more in payroll contributions but potentially pay less overall for care, the Classic PPO option might be the best fit for you. This option has the higher contribution from your paycheck, but a lower deductible. This means the Medical Plan will pay more for eligible expenses sooner.

- If you prefer to pay less in payroll contributions but potentially more overall for care, the HSA-Compatible PPO option might be the best fit for you. It has the higher deductible, so the Medical Plan begins paying benefits for eligible expenses later. But the costs taken out of each paycheck will be lower.

Have you used your medical coverage this year?

Consider how you and your family members have used your medical coverage so far this plan year. Based on your personal situation and upcoming health care needs and preferences, decide which of the medical options—Classic PPO or HSA-Compatible PPO—might be best for you.

If you or a covered family member:

- Go to the doctor quite a bit, including visits with a specialist

- Plan to take part in activities that could result in an accident or injury

- Have a major surgery planned for next year

… then the Classic PPO option might be right for you.

If instead, you or a covered family member:

- Mostly need preventive care and regular immunizations

- Don’t often visit the doctor for illness/injury

- Don’t have planned major health care needs for next year

… then the HSA-Compatible PPO option might be right for you.

Who do you need to cover?

As an eligible employee, you can cover your dependents, including your:

- Legal spouse

- Same- or opposite-sex domestic partner

- Child(ren)

Consider whether it makes sense for you and your family to be covered under the Medical Plan or through your spouse’s/domestic partner’s employer (if applicable).

Looking for more details?

You can access more detailed coverage information, including provider finder tools on MyBenefits Online.