Medical

comprehensive coverage for certain services—including in-network preventive care covered at 100%

The Mondelēz Global Medical Plan (Medical Plan) offers coverage options and carrier options:

- Three coverage options (see side-by-side comparison), with two of them paired with a Health Savings Account (HSA). You can use an HSA to help pay for eligible expenses on a tax-free basis (see the HSA page for details).

- Up to four carrier options, depending on which carriers are available in your area. Carriers may include Aetna, Blue Cross and Blue Shield of Illinois (BCBS), Cigna, and Kaiser Permanente (California only). Some carriers aren't available in all areas. And, if you live in Hawaii, coverage is through HMSA (see details on MyBenefits Online).

Log in to your MyBenefits Online account to see your current coverage elections and for additional coverage and carrier-related details.

Note that all coverage options include prescription drug coverage through retail and mail order programs. Prescription drug coverage is through CVS Caremark (except where Kaiser Permanente and HMSA are the carriers).

Key Features

The $750, $2,250, and $3,500 Deductible options have key features.

How the coverage options are the same

- Covered services: All three coverage options provide comprehensive coverage for the same medical services, such as doctor office visits and hospital stays.

- Carrier options: Same carriers are available under all three coverage options, all with high-quality provider networks.

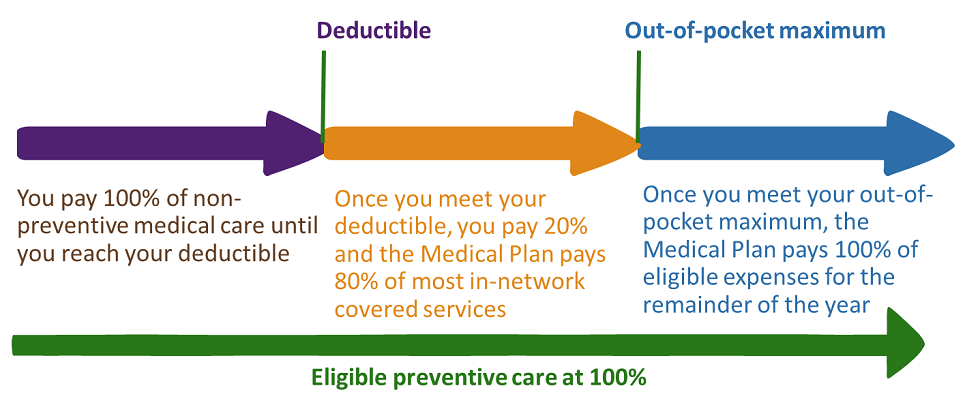

- Preventive care coverage: In-network preventive care is covered at 100% (e.g., annual physical, mammogram, well-child care).

- Medical coinsurance amount: After reaching the deductible, you pay 20% coinsurance for most covered services until reaching the out-of-pocket maximum (then you pay nothing).

- Prescription drug coinsurance/copay amounts (retail pharmacy): For a 30-day supply, pay a maximum of $15 for Generic, 30% coinsurance for Preferred Brand ($35 min/$85 max) and 40% coinsurance for Non-Preferred Brand ($60 min/$110 max). Under all three coverage options, you must satisfy the deductible first before these cost-sharing amounts apply. Out-of-network prescription drug services aren’t covered under any of the coverage options.

How they are different

Here's a quick comparison. For the full details, check out the side-by-side comparison.

| Features | $750 Deductible | $2,250 Deductible | $3,500 Deductible |

|---|---|---|---|

| Pay up-front. You pay more in contributions, but have a lower deductible, so generally pay less out of pocket when you need care. | ✓ | ||

| Pay as you go. You have lower monthly contributions, but a higher deductible, so you generally pay more out of pocket if/when you need care. | ✓ | ✓ | |

| Save with an HSA. Coverage is paired with an HSA to help pay for out-of-pocket costs and/or save for the future—all tax free. | ✓ | ✓ | |

| Use the Health Care FSA to save on taxes. Money you don’t use for eligible expenses during the year will be forfeited. | ✓ | ||

| Pay the deductible first for prescriptions. After the deductible, you pay the same fixed-dollar copay or a percentage of the cost, depending on the type of prescription. | ✓ | ✓ | ✓ |

About the Carrier Networks

Each carrier has its own network of providers. And, when you stay in-network, covered services are provided at a discount. It’s important to note that there are three types of networks across the carrier options, and they’re not the same:

- Broad network: Includes a larger selection of providers, for example more doctors and hospitals, across the country.

- Select network: Includes a smaller group of providers, also referred to as High Performance Networks (HPNs). If a select network is available in your area and your provider is in-network, your contribution amount is generally lower.

- Regional network: Kaiser Permanente is the only carrier option that offers this type of network. If you elect this carrier, you need to receive care from in-network providers (except in the case of an emergency). If you don’t, your services won’t be covered.

Here’s a snapshot of the carrier options, type of network offered by each (broad, select, or regional), and the name of each network by carrier.

| Carrier Option | Type of Network | Network Name | More About the Network |

|---|---|---|---|

| Aetna | Broad | Aetna Choice POS II | Offered in Non-Premier Network Areas |

| Select | Aetna Premier Care Network (APCN) | Available Only in Certain Areas | |

| Blue Cross and Blue Shield of Illinois | Broad | Blue Card PPO, BCBS Select Networks | Available Depending on Location |

| Cigna | Broad | Open Access Plus | Offered in Non-LocalPlus Network Areas |

| Select | Cigna LocalPlus | Available Only in Certain Areas | |

| Kaiser Permanente | Regional | Regional Networks are Offered Where Kaiser Permanente is Available | |

To confirm whether your doctor, hospital, or other care provider participates in a carrier’s network (and whether the network is a broad or select network), be sure to use the provider look-up tool on MyBenefits Online. Before you decide on a carrier, it’s also a good idea to double-check directly with your provider to make sure they participate in a carrier’s broad, select, or regional network where you live. Your provider will have the most up-to-date information about their participation in the carrier networks.

How you pay for care

To decide what's right for you, take a close look at your costs and consider how you prefer to pay for coverage.

- Paying more up-front means you'll have higher contributions, but coverage will begin sooner (lower deductible and out-of-pocket maximum).

- Paying as you go means your contributions will be lower, but it will take longer for coverage to begin (higher deductible and out-of-pocket maximum).

Here's how the options compare against some of the key features that affect how and when you pay for care:

| $750 Deductible | $2,250 Deductible | $3,500 Deductible | |

|---|---|---|---|

| Contributions | Highest | Medium | Lowest |

| Deductible that must be met up-front | Lowest | Medium | Highest |

| What the Medical Plan pays after the deductible is met (for most covered services) | 80% | 80% | 80% |

| Out-of-pocket maximum amount | Lowest | Medium | Highest |

Need a quick refresher on how you and the Medical Plan—regardless of whether you select the $750, $2,250, or $3,500 Deductible option—share in the cost of coverage? Check out the graphic below.

Family Coverage

If you cover family members, it’s important to understand how the deductibles and out-of-pocket maximums work—it affects when the Medical Plan’s benefits kick in.

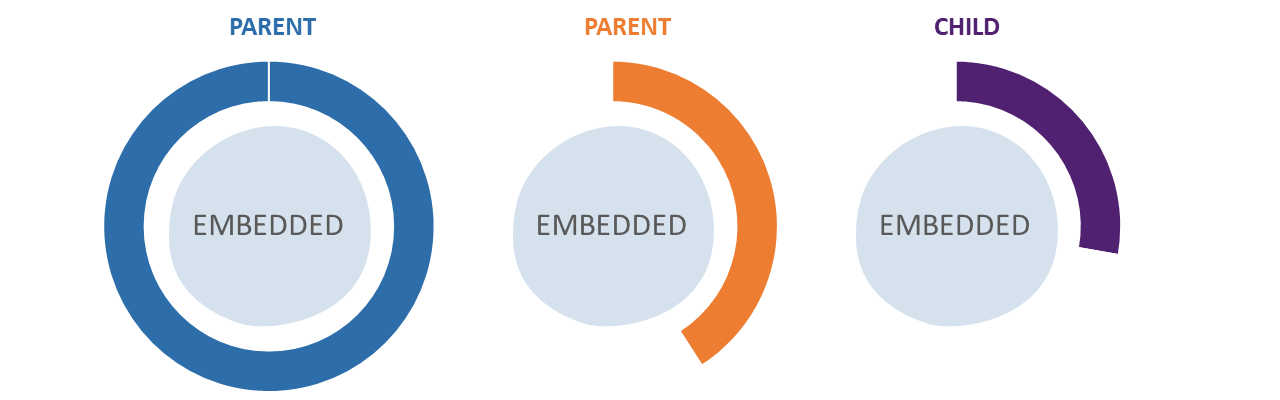

Embedded

The $750 and $3,500 Deductible options have an embedded approach to the deductible, which is the more traditional way of thinking about deductibles. With this approach, once one family member meets their individual deductible, it’s considered met for that person. Benefits begin for them, but not yet for the other family members. This means:

- Each person only needs to meet the individual deductible before the Medical Plan begins paying benefits for that individual.

- Other covered family members will continue to pay all of their health care expenses until two or more combined meet the family deductible. When that happens, the Medical Plan then begins paying benefits for all covered family members.

- If you have a family member who tends to have more health care costs than the others, you might want to consider choosing an option with this approach, as it could save you money.

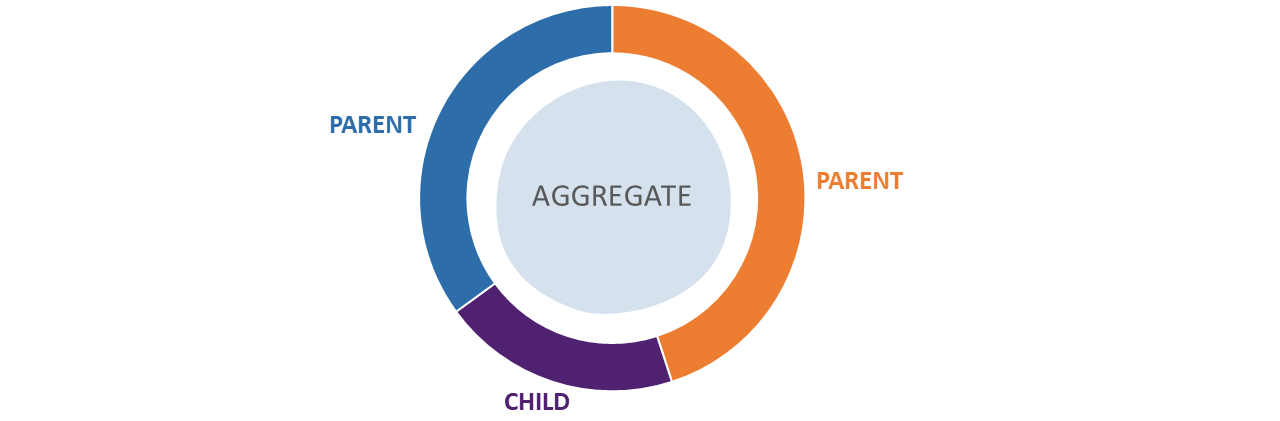

Aggregate

In order to meet IRS rules to be paired with an HSA, the $2,250 Deductible option has an aggregate approach to the deductible. With this approach, there’s one deductible for the whole family. This means:

- You ignore the individual deductible amount completely.

- Only the family deductible applies to each covered family member.

- Once one person or a combination of covered family members meet the deductible, it’s considered met for all covered family members and benefits begin for everyone.

Out-of-pocket maximums under the embedded and aggregate approaches work the same way as the deductibles do for each method.

Telemedicine

With telemedicine, you can talk to a doctor 24/7. Each carrier offers telemedicine for a variety of services (e.g., general medical, behavioral/mental health). Per-visit costs vary by carrier and type of service received; but are often less than what you would pay for in-office care.

For specifics on telemedicine options and costs, contact the carriers directly:

- Aetna: 1-855-835-2362 | Teladoc Website

- BCBS: 1-800-770-4622 | MD Live Website

- Cigna: 1-888-726-3171 | Cigna Website

- Kaiser Permanente (California Only): 1-866-454-8855 (Northern California) | 1-833-574-2273 (Southern California) | Kaiser Permanente Website

Learn more about telemedicine in this video.

Tobacco Surcharge & Carrier Processes

Tobacco user surcharge may apply

You’ll pay less for your medical coverage if you don’t use tobacco. An additional $100 monthly surcharge will apply for you (not covered dependents) if you use tobacco products of any kind (including e-cigarettes or anything that reasonably resembles tobacco products), no matter how frequent the use. If you enroll in coverage through MDLZ, you’ll be asked to certify your tobacco-use status during enrollment. Penalties, termination of coverage, and employment-related discipline may apply if you don't truthfully report your tobacco-use status.

If you complete a smoking cessation program offered through one of the medical or prescription drug carriers under the Medical Plan (or outside the Medical Plan), the additional monthly surcharge won’t apply. See the “Your Guide to the Mondelēz Global LLC Group Benefits Plan” for details on how to attest your non-tobacco-use status (access the Guide in the Reference Center on MyBenefits Online).

Processes and standards vary by carrier

Two carriers may treat a covered service differently when making a benefit determination. As a result, how services are covered and what you may pay can vary across carriers. Also, carriers might adjust costs for certain services (for example, negotiated rates for certain covered services and telemedicine costs) from year to year. If you have questions about how a specific service is covered, contact the carrier directly.

Contact info & apps

Aetna

- Aetna Website

- Teladoc Website

- Main Phone: 1-866-831-0051

- Telemedicine: 1-855-835-2362

- Nurseline: 1-800-556-1555

- Mobile App: APPLE APP STORE | GOOGLE PLAY STORE

- Group Number: 868605

- Network:

- Select: Aetna Premier Care (only available in certain areas)

- Broad: Aetna Choice POS II (offered in non-Premier network areas)

Blue Cross and Blue Shield of Illinois (BCBS)

- BCBS of Illinois Website

- MD Live Website

- Main Phone: 1-877-238-5948

- Telemedicine: 1-800-770-4622

- Nurseline: 1-800-299-0274

- Main Phone: 1-877-238-5948

- Mobile App: APPLE APP STORE | GOOGLE PLAY STORE

- Group Number: See your member ID card

- Network: Broad—Blue Card PPO or Blues Alternate Networks (depending on location)

Cigna

- Cigna Website

- Cigna Telemedicine Website

- Main Phone: 1-800-244-6224

- Telemedicine: 1-888-726-3171

- Nurseline: 1-800-564-9286

- Mobile App: APPLE APP STORE | GOOGLE PLAY STORE

- Group Number: 3341199 or 2500546

- Network:

- Select: Cigna LocalPlus (only available in certain areas)

- Broad: Open Access Plus (offered in non-LocalPlus network areas)

Kaiser Permanente (California Only)

- Kaiser Permanente Website

- Kaiser Permanente Telemedicine

- Main Phone: 1-800-464-4000

- Telemedicine: 1-866-454-8855 (Northern California) or 1-833-574-2273 (Southern California)

- Nurseline: Contact Kaiser Permanente at 1-800-464-4000 or access the Get Care Now Program at kp.org/choosebetter

- Mobile App: APPLE APP STORE | GOOGLE PLAY STORE

- Group Number:

- Northern California: 608105

- Southern California: 236674

Short videos you may find helpful

Check out these videos to learn more about how to:

Key Considerations when choosing medical coverage

How and when do you prefer to pay for medical coverage?

- If you prefer to pay more in up-front contributions and potentially pay less overall for care, the $750 Deductible option might be the best fit for you. This option has the highest contribution, but the lowest deductible. This means more will be taken out of each paycheck, but the Medical Plan will begin paying benefits sooner.

- If you prefer to pay less in up-front contributions but potentially pay more overall for care, the $3,500 Deductible option might be the best fit for you.

- The $2,250 Deductible option is in the middle, balancing up-front contributions and when the Medical Plan begins to pay benefits.

COVERAGE OPTIONS IN ACTION

Let’s take a look at an example. Mark is injury-prone so he prefers to pay less at the time of care. He falls off his bike, breaks his leg, and unfortunately ends up with a $3,000 hospital bill. This is Mark's first time needing medical care this year, so he hasn't had any out-of-pocket expenses applied toward his annual deductible.

If Mark has coverage for himself only, his medical costs would be as follows:

| $750 Deductible option | ||

|---|---|---|

| $750 (Out-of-pocket costs to reach deductible) | + $450 ($2,250 Remaining x 20% coinsurance) | = $1,200: Total costs + Highest contributions |

| $2,250 Deductible option | ||

|---|---|---|

| $2,250 (Out-of-pocket costs to reach deductible) | + $150 ($750 Remaining x 20% coinsurance) | = $2,400: Total costs + Middle contributions |

| $3,500 Deductible option | |

|---|---|

| $3,000 (Out-of-pocket costs toward his deductible) | = $3,000: Total costs + Lowest contributions |

Given that Mark is injury-prone and might have a few accidents that require seeing a doctor in the future, he may want to consider paying higher contributions for the $750 Deductible option so that his benefits kick in sooner. When making your decision, consider how often you may need health care plus your contributions.

Have you used your medical coverage this year?

Consider how you and your family members have used your medical coverage so far this plan year. Based on your personal situation and upcoming health care needs and preferences, decide which of the medical options—$750, $2,250, or $3,500 Deductible—might be best for you.

If you or a covered family member:

- Go to the doctor quite a bit, including visits with a specialist

- Plan to take part in activities that could result in an accident or injury

- Have a major surgery planned for next year

...then the $750 Deductible option might be right for you.

If instead, you or a covered family member:

- Mostly need preventive care and regular immunizations

- Don't often visit the doctor for illness/injury

- Don't have planned major health care needs for next year

...then the $2,250 or $3,500 Deductible options might be right for you.

Who do you need to cover?

As an eligible employee, you can cover your dependents, including your:

- Legal spouse

- Same- or opposite-sex domestic partner

- Child(ren)

Consider whether it makes sense for you and your family to be covered under the Medical Plan or through your spouse's/domestic partner's employer (if applicable).

What contributes to your cost for medical coverage?

Estimating your total costs and considering your budget can help you determine which medical option makes the most sense for your situation.

Your costs depend on:

- Medical option you select: You'll pay less in contributions and more at the time of care ($2,250 or $3,500 Deductible option) or more in contributions and less at the time of care ($750 Deductible), depending on the option you elect.

- Carrier you select: Choosing a carrier with your preferred doctors and hospitals in that carrier's network can save you money. Note: Some carriers aren't available in all areas.

- Type of network you select: You can have lower contributions deducted from your paycheck if you choose a network with a smaller group of providers (also called a select network if offered in your area). If you prefer a larger selection of providers, consider what's often referred to as a broad network option.

- Who you need to cover: The number of family members you cover impacts your contribution amount from your paycheck. The more people you cover, the more you pay.

Need help choosing? Not sure which coverage is a good fit for you and your family? Choose I'd Like Help Choosing Plans when you enroll and answer a few questions to find what best fits your unique coverage needs. Results are based on your answers and are completely confidential.

Looking for more details?

You can access more detailed coverage information, including provider finder tools on MyBenefits Online.